DailyAIWire | AI News | Markets

Part of Sterlite’s rise is backed by tangible progress—a major order win and a return to profitability. The rest appears to reflect growing market optimism and higher expectations. Both have fueled the rally, but only the business fundamentals provide a firmer foundation.

The spotlight is firmly on Sterlite Technologies, the optical-fibre manufacturer associated with billionaire Anil Agarwal’s Vedanta group. Much of the excitement centers on the claim that ₹1 lakh turned into nearly ₹6 lakh over a short period. Still, the stock’s sharp rise is tied to specific developments, and understanding those details is just as important as appreciating the returns.

The number, and why it depends on where you start

Sterlite Technologies, which trades on the NSE as STLTECH, is up more than 500% in 2026. Zee Business reported the stock at ₹619.05 on June 5, a gain of about 504% so far this year and more than 720% over twelve months.

Be careful with that headline figure, because the baseline changes it. Measured from January 1, the year-to-date gain was closer to 352% in late May, per Business Standard. Measured from the stock’s 2026 low of ₹84.60 on January 27, the rise is around 550%. All three numbers are real. They just answer different questions, and the most dramatic one, the move off the low, is the one that flatters the story most.

What actually triggered the run

The key catalyst behind the rally is one major order. On May 22, Sterlite disclosed a multi-year Product Award Letter valued at over $1 billion (approximately ₹10,000 crore) from a US-based hyperscaler building AI data centres. Scheduled to run between FY2027 and FY2029, the deal will see the company’s optical products deployed in US AI infrastructure.

Sterlite has not disclosed the identity of the customer, a notable omission given that the undisclosed counterparty underpins much of the stock’s roughly 550% surge. While the company announced a contract worth more than $1 billion, the associated revenue is still expected to be recognized over future years rather than immediately. Managing Director Ankit Agarwal said the agreement positions Sterlite as the provider of the connectivity backbone for the client’s AI data centres. To strengthen its presence in this market, the company has also introduced a dedicated data-centre portfolio under the STL Neuralis brand.

Investors are looking at more than just one blockbuster deal. In the March quarter of FY26, Sterlite reported revenue of about ₹1,441 crore, a 37% increase from a year earlier, and reversed a ₹40 crore loss into a ₹59 crore profit. The shift to sustained profitability may ultimately be a more important factor for the company’s future than its recent share-price surge.

The part the clone articles skip

Here is the framing a reporter owes you that “do you own?” headlines do not.

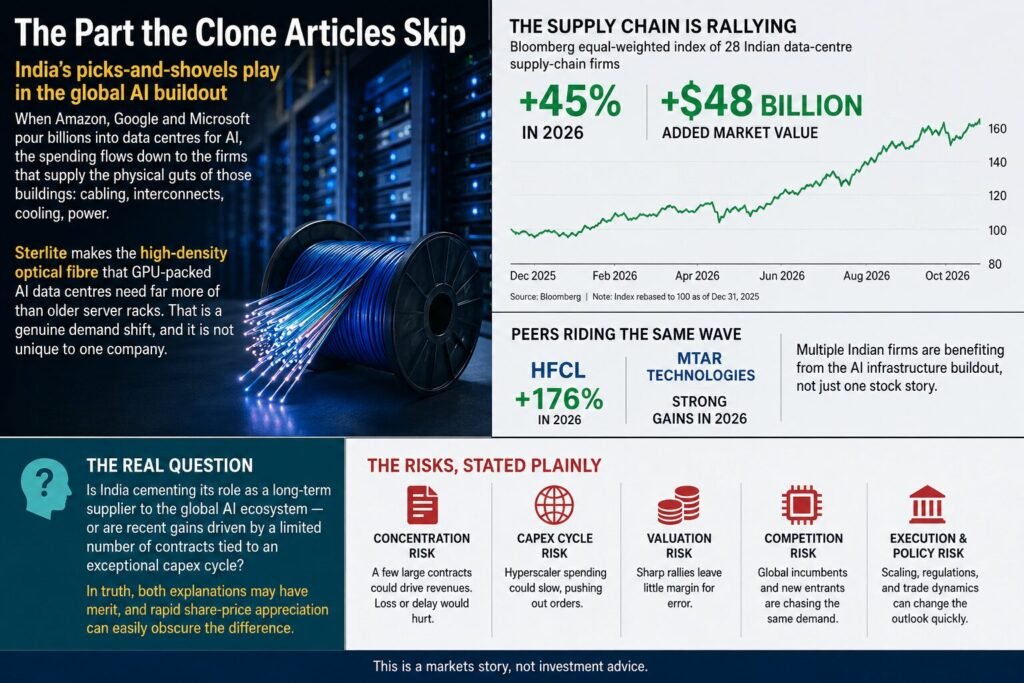

This is the “picks and shovels” trade reaching India. When Amazon, Google and Microsoft pour billions into data centres for AI, the spending flows down to the firms that supply the physical guts of those buildings: cabling, interconnects, cooling, power. Sterlite makes the high-density optical fibre that GPU-packed AI data centres need far more of than older server racks. That is a genuine demand shift, and it is not unique to one company. A Bloomberg equal-weighted index of 28 Indian data-centre supply-chain firms has gained about 45% in 2026, adding close to $48 billion in market value. Peers such as HFCL and MTAR Technologies have risen on the same wave, with HFCL up about 176% for the year.

The key issue is not whether Sterlite belongs in the AI category. It is whether India is cementing its role as a long-term supplier to the global AI ecosystem or whether recent gains reflect a limited number of contracts tied to an exceptional capex cycle. In truth, both explanations may have merit, and rapid share-price appreciation can easily obscure the difference.

The risks, stated plainly

A 550% run on a small-cap concentrates several risks that the excitement tends to bury.

The order book is not revenue until it is delivered, and delivery spans FY27 to FY29, years away, with execution risk attached. The biggest catalyst comes from an unnamed client, so there is little independent visibility into it. Small-cap stocks that re-rate this fast tend to move just as hard in reverse when momentum fades, and the valuation now prices in a long stretch of near-flawless execution. None of that means the business is weak. It means the share price has already paid forward a lot of good news.

I report on this sector; I do not give investment advice, and nothing here is a recommendation to buy or sell. The useful takeaway is narrower than the headlines suggest. Sterlite has a real order, a real return to profit, and a real tailwind from AI infrastructure spending. It also has a price that has run far ahead of delivered results, on a catalyst it has not fully disclosed. Anyone deciding what to do with that should weigh the order book against the execution risk, and talk to a qualified adviser, rather than act on a 500% number in a headline.

What to watch next

- Delivery, not announcements. The first signs of the $1 billion order converting into booked revenue from FY27 will matter more than any further price spike.

- Whether Sterlite or its client names the counterparty. Disclosure would reduce the biggest uncertainty in the story.

- The wider data-centre supply index. If the whole basket cools, Sterlite is unlikely to hold up alone.

Leave a Reply